Regular readers of this page know that I have written multiple posts on the general topic of privacy concerns with online ad targeting. More recently, I have highlighted a lower-profile, but equally important facet of the privacy discussion: data ownership.

2010 was a turning point in the data ownership/privacy discussion. So as 2011 kicks off, I thought it would be worthwhile spending a moment to tie these threads together in the context of the digital advertising value chain.

The value chain begins with users, who move from publisher to publisher and page to page consuming content that interests them. In most cases publishers provide this content free of charge in exchange for the opportunity to present ads to users who consume it. Publishers then sell the ad inventory so created directly to media agencies (who buy on behalf of advertisers) or through some mix intermediaries including SSPs, exchanges, DSPs and Ad Networks.

Increasingly, agencies are choosing to buy (and thus publishers – sometimes reluctantly – are choosing to sell) through intermediaries. Therefore, the value chain for a typical advertising transaction is as follows: user, publisher, ad network or DSP, agency, advertiser.

Sitting in the middle of this value chain are ad networks and DSPs. As has been discussed, it’s often difficult to assign a given company cleanly to one bucket or the other, but this link in the chain generally aggregates publisher ad inventory and agency demand, providing agencies with targeting and optimization capabilities and increasing operational efficiency for both publishers and agencies.

Here’s a typical example:

A network or DSP runs a campaign for an eyeliner product from a large CPG advertiser on a group of womens’ content sites. The network/DSP collects data on which users it encountered on which sites or site sections (e.g., beauty tips, product reviews), who clicked on and/or engaged with the eyeliner ad and on which publisher pages/sites they did so. Depending on how the campaign is configured and measured, the network/DSP may even collect some activity data from the advertiser’s site. The network/DSP then turns around and sells media based on that data – say by a) retargeting those users on other sites or b) offering those users or look-alike users to other advertisers or c) some combination of both.

The activities this example illustrates are commonplace, but the appropriate legal permissions for this type of data use are almost never explicitly granted today. In fact, in many cases some or all of these activities are expressly prohibited. Like users who are becoming increasingly concerned about the extent to which data about them and their behavior has been bought and sold without their knowledge, many advertisers and publishers would be surprised (shocked) at how their data is being used.

Which brings me back to the value chain.

Of all the entities in this value chain – user, publisher, network or DSP, agency, advertiser – intuitively, which entities have the strongest claims to ownership of the valuable data generated by an online ad campaign? I would argue that the ends of the value chain – the user and the advertiser – have the strongest claim to ownership of this data, with other parties’ claims weakening dramatically from the ends to the middle. Who has more rights in a user’s behavioral data than that user? Who has more rights in an advertiser’s performance data than the advertiser who paid for the campaign? It’s patently obvious.

Of course, these data owners may choose to license some of their inherent rights to others in exchange for something of value. For example, a user may be OK with a publisher recording and using his browsing habits to deliver more targeted content or sell ads to subsidize free content. Or an advertiser might be OK with their agency recording and using ad performance data to improve the return of their campaigns over time.

However, in full knowledge and understanding, would the average user really be OK with an ad network or DSP, with whom the user has no relationship, constructing a comprehensive view of her life (anonymous or not) and selling those details to the highest bidder?

The industry generally defends this practice by extolling the user value of relevant advertising. This argument has been proven valid in Search advertising, but is a tenuous proposition at best in Display. Regardless, each user should make the decision on the value of ad relevance vs. privacy, not the industry on behalf of all users.

Similarly, would the average advertiser be OK with an ad network or DSP using data about how its campaigns perform to improve performance of direct competitors’ campaigns? I’m not sure what the industry’s “pro-data-owner” argument would even be in this case. Yet, again, this type of activity is routine in today’s digital ad market.

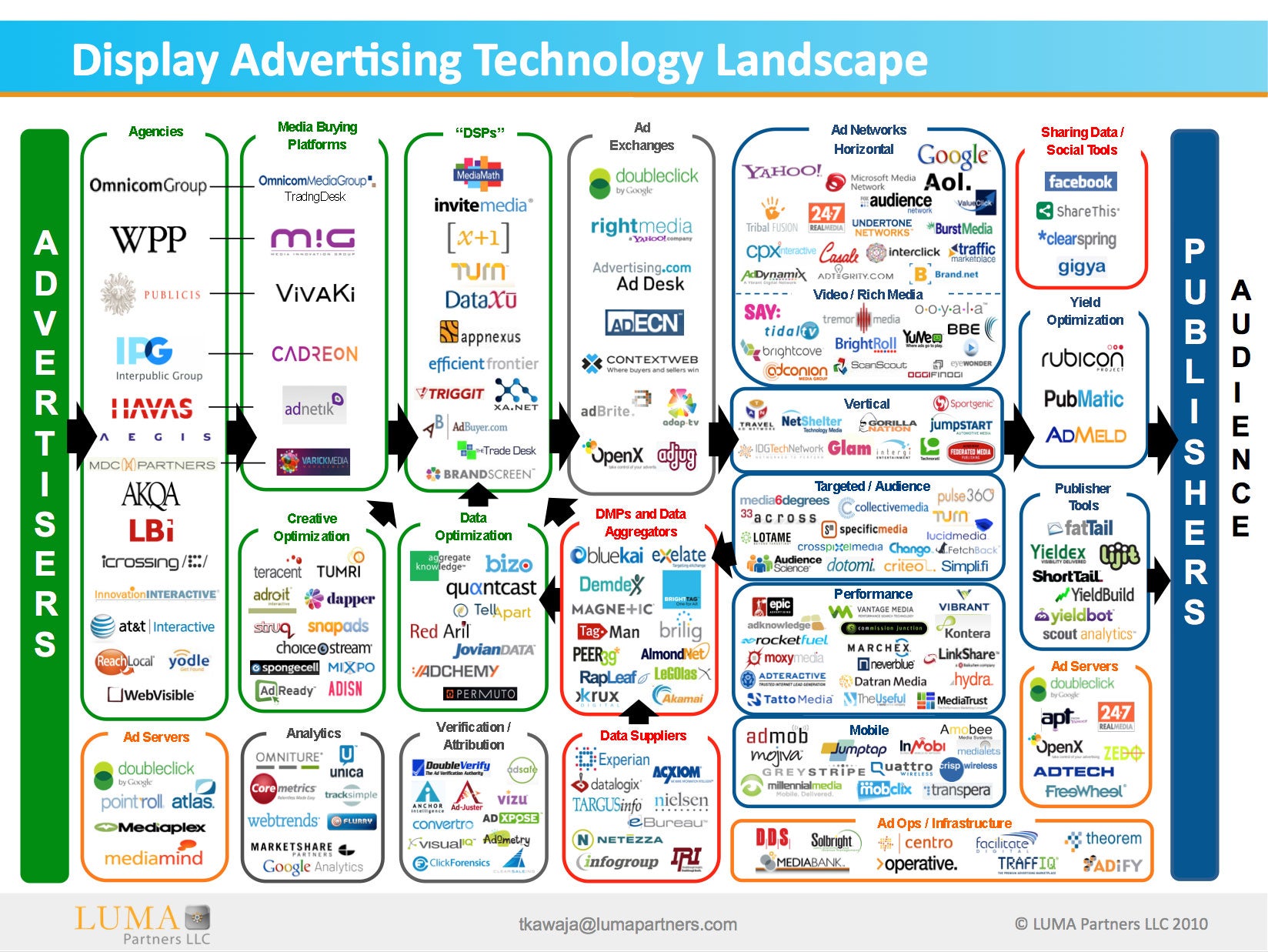

So I would argue that the privacy debate that rages today is fundamentally a reflection of the simple property rights issues these activities raise. Users and advertisers at the ends of the value chain own the data, but that data is being used and monetized primarily by the players in the middle of the value chain. The vast majority of this data use and monetization is unlicensed, representing a free ride on the gravy train for about half of the companies on LUMA Partners’ ubiquitous landscape chart.

The government appears to be leaning towards addressing this set of issues on behalf of users with a “do not track” list, but even without do not track – as many are skeptical of the speed of government to act – the private sector is rapidly innovating. New versions of browsers from Microsoft and Mozilla will ship with privacy protections built-in. For those who don’t want to upgrade, browser extensions are also providing private, user-controlled do not track capability. Another new technology, from Bynamite, is taking a different approach by providing the user a way to control – and profit from – distribution of their data.

In defense of corporate data owners, companies like Krux Digital are providing tools to help publishers keep from getting their virtual pockets picked. I am not aware of any company providing similar data security audit solutions for advertisers, but this is an essential technology representing a huge opportunity. I am sure a solution is on the way.

The landscape is evolving quickly and it’s still unclear as to how it all will end up, but one thing is certain. The long term solutions to the “privacy” issue will give data owners at each end of the value chain dramatically increased visibility of, control over and stake in how their data is used by players in the middle.

And as these capabilities allow the data gravy train to begin charging for tickets, you’re going to see fewer riders.

{kind=link}