There was a really interesting article in Ad Age last week that underscored the increasingly important role of corporate procurement, or strategic sourcing, groups in the media buying process.

This is not a new development by any means. We first referenced this trend on this page last year and it began years before that. However, the appointment of a formal ANA task force designed to improve the relationship between procurement groups and their partners – in this case marketing teams and agencies – shows how far this trend has gone.

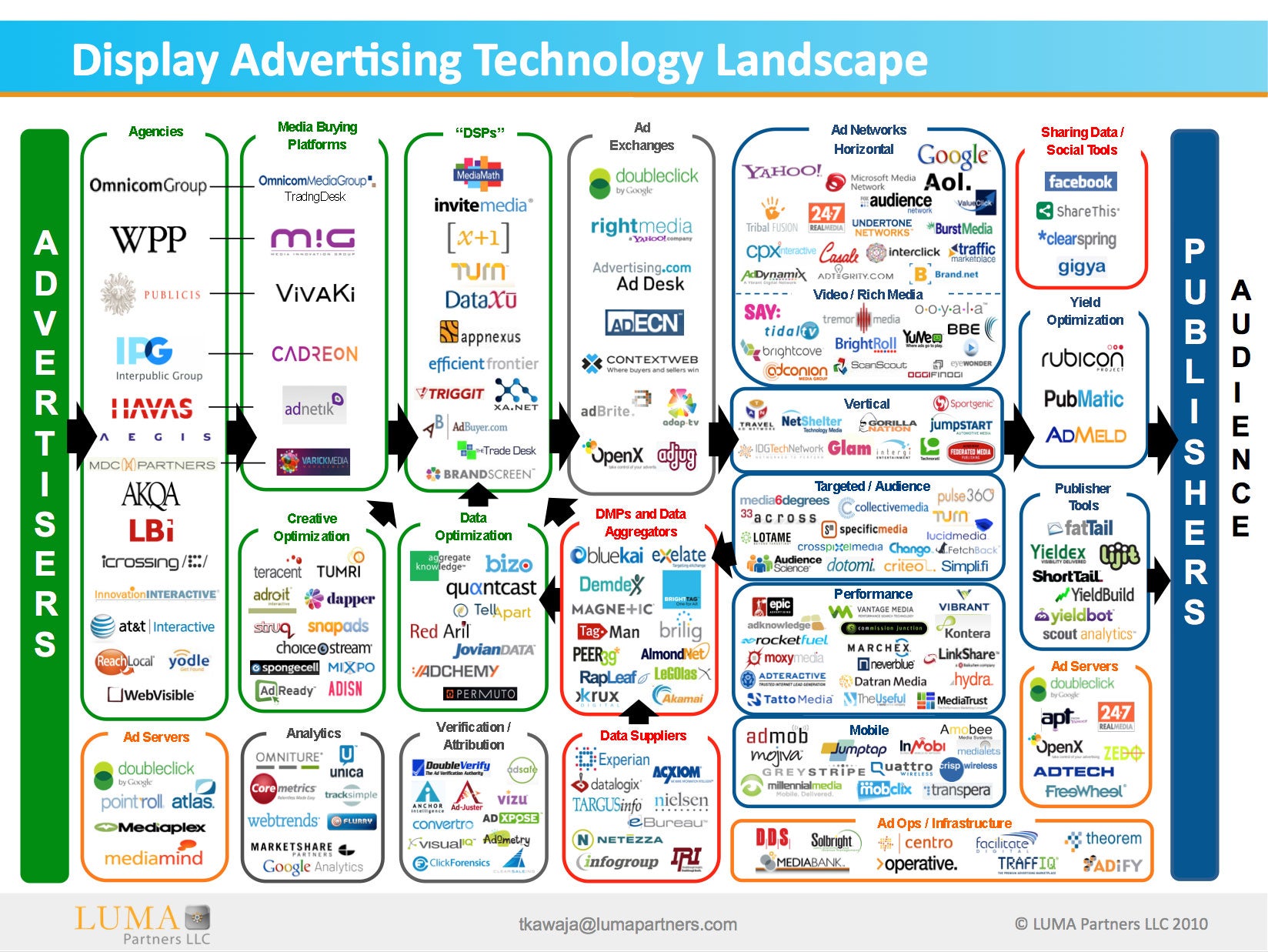

The boxes are unpacked and the renovations have started. The new neighbors are here to stay.

One might ask why such a task force is necessary. One study, for example, presents a pretty stark picture of the need. There’s clearly a significant perception gap between procurement groups, marketing groups and agencies; each has a very different perspective on the role and value add of the others.

Procurement teams see their role as constructive. Their involvement helps improve the return on a critical corporate investment with a focus on increasing value rather than reducing cost, a view clearly expressed in this Q&A with several prominent procurement executives.

But according to the study results, agencies and marketing teams apparently do not unanimously agree. Marketing teams and agencies clearly feel that procurement can err on the side of the numbers, ignoring important qualitative, creative or relationship factors. There are also perceived skill gaps; only 14% of agency executives, for instance, said procurement “is knowledgeable in advertising/marketing”.

The ANA task force appears dedicated to ironing out these differences in perception to improve the efficiency and tranquility of the “neighborhood”, if you will. Part of their remit is to help procurement teams get up the learning curve quickly on what for some is a new domain – marketing. There will also no doubt be attention paid to focusing procurement efforts on areas where they can add the most value the fastest. Getting points on the board quickly is a key ingredient to successful change management.

To that end, I think there are some helpful suggestions in another Ad Age article. The author casts procurement as a tool to help marketers and agencies build working budgets by improving efficiency, accountability and control. That’s a state I think all constituents would agree represents success.

Renegotiating agency compensation is one thing on which the three constituencies could reasonably have tension. But there are many issues on which agreement should be fairly straightforward. Would anyone argue against a lean, streamlined briefing process, or for travel when Webex would suffice? Does one account really need a sprawl of different agencies? These seem like relatively obvious areas where experienced procurement practitioners can leverage experience from other domains to deliver significant savings that could be channeled back into working media budgets.

Even more strategic would be leveraging procurement’s experience in sourcing other direct and indirect materials to drive improvements to the processes for planning and sourcing media – particularly in digital. As the author mentions, this is an area of great potential due to its rapidly growing share of budget and the extreme complexity in today’s digital process/ecosystem.

I couldn’t agree more, but as I mentioned in my own Ad Age article, procurement teams need new technology to help them add this value. Accurate forecasts, meaningful delivery commitments, guaranteed quality – these are all indispensible tools to help procurement teams do what they do best in other domains. These capabilities are just as critical in digital media, but the solutions have been sorely lacking.

One author goes so far as to suggest we replace the entire process (procurement, agencies, marketing – apparently the whole kit and caboodle) with what would have to be the worlds gnarliest optimization model. You know when you’re comparing the complexity of your model to those that (attempt to) predict the weather you’re off to a bad start. But even if all the neat stuff described in this futuristic piece was possible today, you’d still need accurate forecasts of capacity and price, and the ability to reliably deliver against forecasts to get real value out of this magic box.

My personal advice is for the incumbents in the media value chain to welcome procurement. In my experience, procurement teams are very much aligned with the objective of helping marketers and agencies build working budgets by improving efficiency, accountability and control. These new partners are smart, focused, disciplined allies that understand that advertising combines art and science. They are here to help.

We’re proud to offer MFP On Demand to all of our customers, particularly the client procurement teams whose needs have largely been ignored by the Silicon Valley (and ‘Alley) technology communities thus far.

{kind=link}