An interesting piece yesterday from Adam Cahill of Hill Holliday, with some great thinking on how to address the quality challenges posed by the evolving real-time digital media landscape.

As Adam correctly points out, for most Brand campaigns delivering results is about more than just protecting a Brand from objectionable content. That itself is very important (and we’re very good at it, by the way), but it’s only the beginning – “necessary, but not sufficient” as they would say back at MIT. Media quality involves not just the the text of a page, but the editorial environment in which it exists. That second bit makes this an even harder technical problem, particularly when you consider that quality is a page-level issue. So we’re currently left with the false choice between audience and content that Adam correctly suggests we reject.

Let’s push a bit further though.

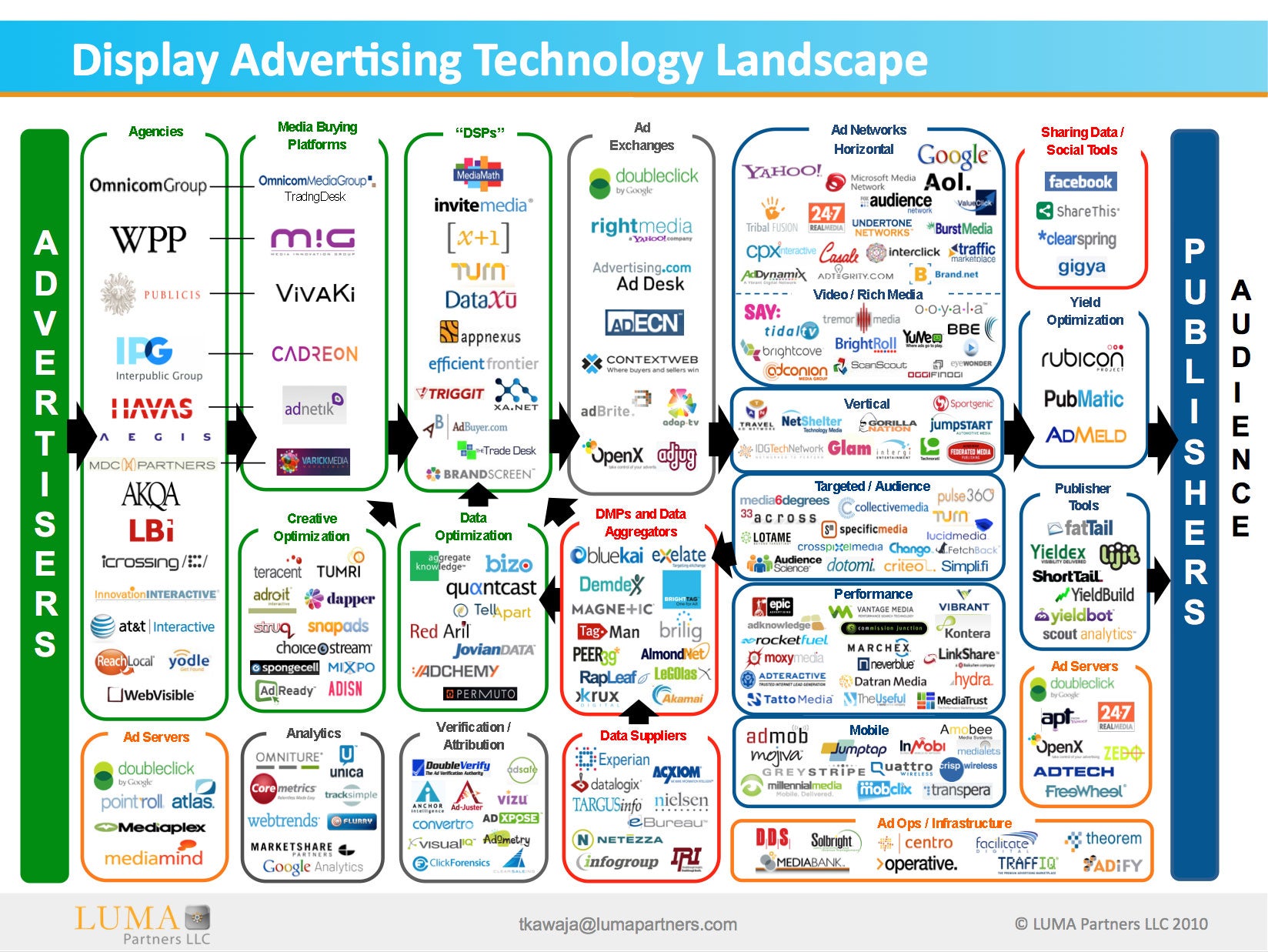

Without taking too much license (Adam, please feel free to chime in), I think I can safely say that “Audiences vs. content” is essentially a compact way of describing the choice between two different operational approaches. “Audiences” is shorthand for scalable, efficient, automated buying via RTB on exchanges. “Content” is shorthand for manual, site-by-site buying. In the rush for operational efficiency, “audience” buying has grown very quickly over the last 2 years while “content” buying has stagnated, resulting in well-documented challenges for many high-quality publishers.

Audience buying works great when fast, high-resolution feedback on a financial goal metric is possible.

For example, let’s assume Netflix’s goal for a big chunk of its marketing spend is profitable subscriber acquisition and they have conversion value and attribution models that they trust. Then, just as long as they have a scalable way of keeping their ads away from damaging content (porn, profanity, etc), they can pretty much ignore the editorial quality / “shades of goodness” issue Adam focuses on in his piece. The tie between editorial quality and performance will show up in the CPA numbers and cause money to move appropriately. So, for this block of DR money, Netflix can optimize based on their conversion metrics and they’re done.

For a brand campaign, the situation is different.

Brand metrics (e.g., awareness, consideration, intent) take longer to measure, they take longer to translate into financial value and that financial value is most often (95% of the time) realized in an offline transaction. This means there is no fast, high-resolution feedback on a financial goal metric for Branding, but the push for enhanced efficiency of audience buying is no less acute. What to do?

Unfortunately, today’s “solution” most often involves substituting for the meaningful data that is lacking some mix of a) meaningless, but conveniently accessible metrics like CTR or b) nice-sounding audience descriptions (like “peanut butter bakers”). Once these substitutions are made, Brand campaigns can smoothly run through the DR-tuned “audience” infrastructure. The problem is that these simplifying substitutions require a huge leap of faith at best and are very often detrimental to performance against the metrics that really matter.

The right way to leverage the new real-time online ad infrastructure for Branding is first to carefully test and measure the impact of different scalable, repeatable targeting criteria on *meaningful* metrics (like purchase intent or offline sales).

This process is conceptually similar to the Netflix example I detailed above; i.e., test, measure, optimize. However, because Brand measurements involve longer time lags and lower resolution, there will need to be some manual effort applied to the process itself before intelligent instructions can be fed into the real-time execution machine. The machine can’t do all the work itself.

It’s an inconvenient truth, but it’s the truth nonetheless.

Unfortunately, these “meaningful, but harder to get” metrics are too often not even gathered today, so the convenient lie persists.

Reading Adam’s article in this context, the richer standards for quality that he’s calling for essentially represent another set of scalable, repeatable targeting criteria added to the mix, one that he expects to have high correlation with results for brand marketers. I wholeheartedly agree there would be a lot of value there. We’ve certainly seen the impact of media quality in our own results.

But I also think it’s important to underscore the higher-level point raised here. In order for the real-time digital ad infrastructure to be complete, it needs native support for branding that is sadly lacking today.

{kind=link}