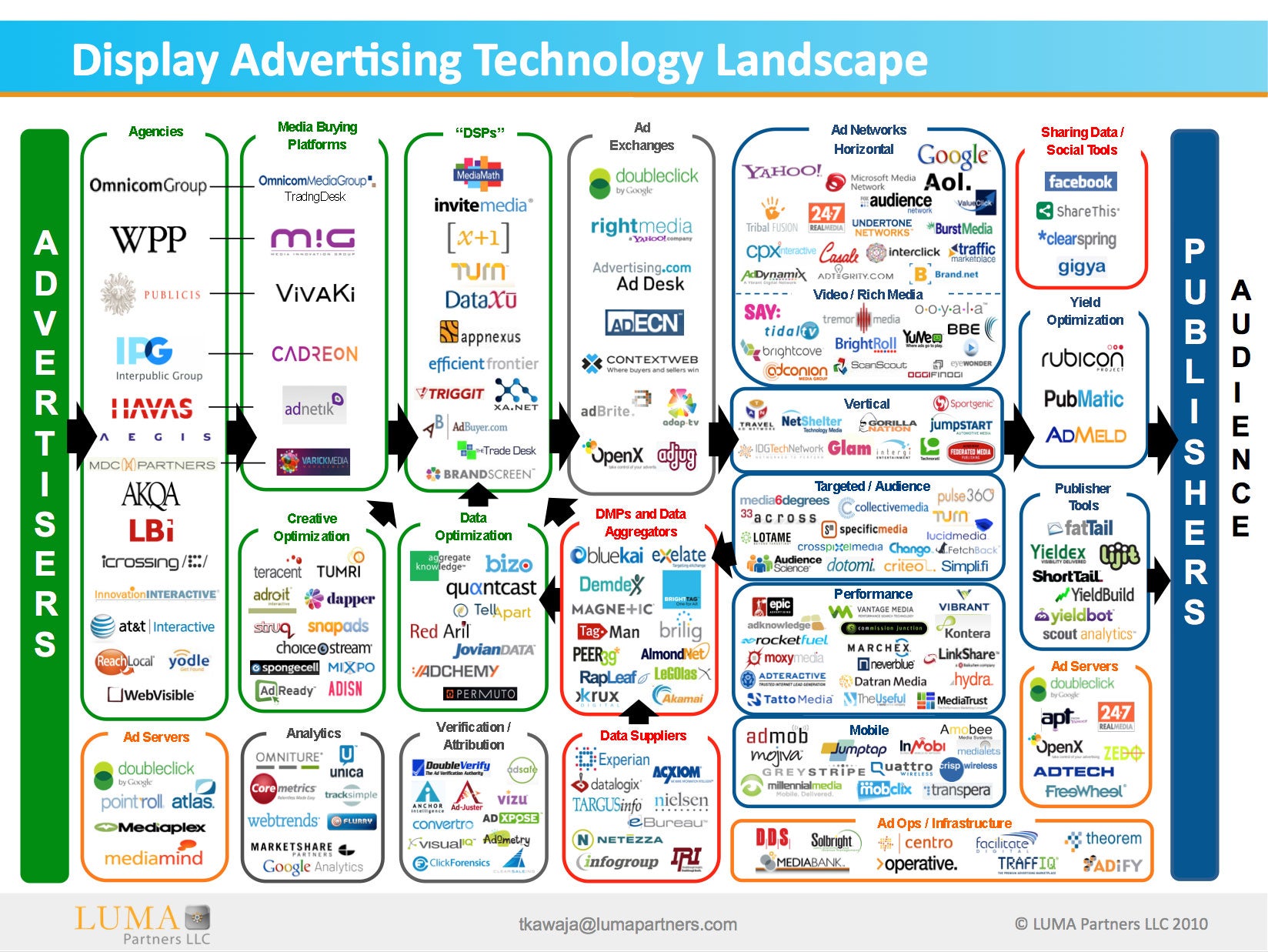

Some very interesting tidbits in Neal Mohan’s post on the Google blog yesterday.

First is that Google sees display inventory per user declining 25% by 2015. This is a pretty interesting prediction given the conventional “wisdom” that online ad inventory is unlimited. This hasn’t ever really been true (provided one cares about quality of placement) and if Neal’s correct, it will become even less true over time as the industry collectively realizes there’s there is too much low quality inventory out there and it’s not doing anyone in the ecosystem – advertisers, publishers or users – any good.

Combine this prediction with the forecast growth in display spend over the next decade and it’s pretty clear we’re heading for a much more constrained inventory landscape. As these constraints start to bite, it will be interesting to see what happens to today’s auction-driven RTB infrastructure where delivery is not guaranteed.

Expect some serious turmoil as delivery rates drop and volatility increases. Maybe that’s why Google has begun work on a reserved inventory product…

I also want to amplify Neal’s point about 35% of campaigns measured on other metrics than clicks and conversions by 2015, particularly offline sales. Those campaigns comprise the orange box on this graphic – some $6B in spend last year. So Neal’s saying the orange share of online spend will grow from just over 20% in 2010 to 35% in 2015.

That prediction certainly syncs with the qualitative discussion in the eMarketer article I cited above, and if you combine the spend estimates there with Neal’s 35% share forecast, you end up with an online brand advertising market of ~$15B in 2015. Using Barclay’s market sizing estimates for the base you end up with ~$18B. So the online brand advertising market will more or less triple by 2015.

That’s great news for the ecosystem as a whole and particularly for the relatively few of us delivering targeted solutions for Brand advertisers.

{kind=link}